Published on August 21st, 2015

IPv4 prices were at an all-time low through the first half of 2015, and then, with the ARIN runout upon us, they spiked upwards. Has the bottom of the IPv4 market occurred, and where prices will go from here?

Let’s start at the beginning. IPv4 Market Group has facilitated over 150 IPv4 transfers through the Regional Internet Registries over 5 years, and from 2011 to the present, prices have generally fallen.

While prices have gone down, the other trend that has become apparent is that price per IP decreases as block size increases. IPv4 Market Group calculated its average price of IPv4 addresses sold over the last five years. The table below clearly shows that across all block sizes, average price per IP has been declining by year. This trend has been consistent since IPv4 Market Group entered the market space in 2011 when the market was in its infancy.

| Block Size | 2011 | 2012 | 2013 | 2014 | 2015 YTD |

| /16 | 10.0 | 10.58 | $9.42 | $7.28 | $6.99 |

| /17 | $10.17 | $8.89 | $7.98 | ||

| /18 | 9.95 | $9.90 | $9.09 | $8.79 | |

| /19 | $11 | $10.58 | $9.03 | ||

| /20 | 15 | $15.30 | $13.63 | $12.18 |

Figure 1. Prices Observed by IPv4 Market Group

Very large blocks trade less frequently, and it would be difficult to state average prices without putting some buyers and sellers at risk of identification, but it is generally accepted that blocks of /13 to /10 have traded at as high as $7.00 per IPv4 address and at as low as $4.00 per IPv4 address.

This says that there is a premium for small blocks and a discount for buying bigger blocks. The reason seems to be because the fixed costs of a transfer, both real and intangible, are spread across fewer IPv4 addresses.

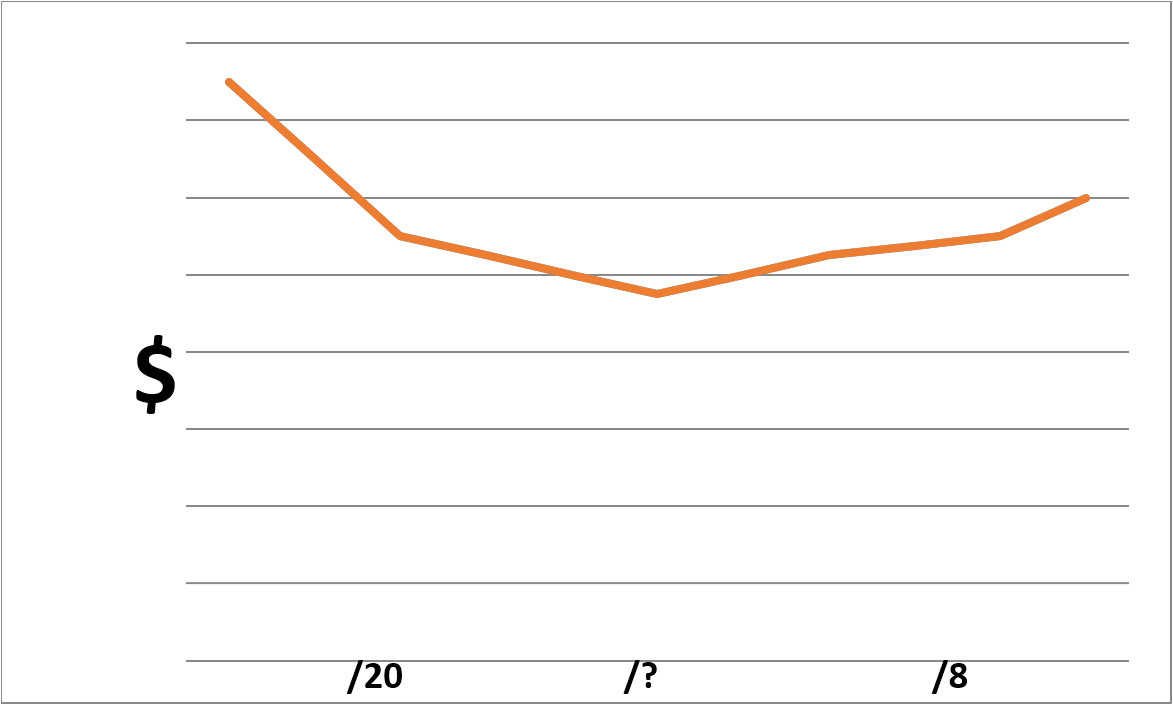

Going forward, IPv4 Market Group foresees two IPv4 market changes: 1) the price decline will reverse, and 2) there will be an inflection in prices as larger blocks become harder to obtain. Large block price increases will outpace medium block price increases as buyers will pay more to get large contiguous blocks.

With ARIN runout, there are no more “free IPs”. The low hanging fruit has already been sold.

With large blocks, in observing the IPv4 marketplace, the low hanging fruit of Merck, Lilly, Dupont, and Nortel have seemingly mostly been sold. This means that the next available large blocks do not appear to be as free or available. The large blocks remaining to be sold either need to be re-IP’d, for which the sellers want more money, or the sellers have simply set a higher price threshold.

Thus, prices are on their way up.

It is difficult to predict where the price inflection point will fall. Because there are many /16’s for sale, it would seem that the price will be less for a /16 than for some blocks larger than a /16 that are extremely rare and contiguous. All we can say is that a /8 block, if available as a whole, could sell for a higher price per IP than a /16.

Figure 2. Shape of IPv4 price curve by block size, small blocks to the left, large blocks to the right

IPv4 Market Group

Should your company buy IPv4 addresses now?

YES!

While dollar cost averaging may be a suitable strategy for most assets, it does not seem appropriate for IPv4 addresses in this market. IPv4 Market Group believes we are at the cusp of a period of increasing prices for at least the next five years. This suggests that a buyer should buy as much as they can, as soon as they can. ARIN runout, global supply and demand, the harmonization of inter-regional transfer policy, and the alignment of price per IP across regions, all point to an inevitable escalation of IPv4 prices. Now is the time to sell your IP address blocks at optimal prices and buy before rates go higher. Contact IPv4 Market Group to facilitate your transfer process today.